RSM recovery watch: Upgraded growth forecast and more evidence of a turn in the business cycle

There are signs that the business cycle has made a turn, bottoming out of a deep recession and moving into its next phase of sustained economic growth. As such, we have recently upgraded our forecast for 2021 real GDP growth to 7.5% (7.2% previously) on a year-over-year basis, a decline in the unemployment rate to 4.1% (4.5% previously) and an increase in demand able to support 10-year Treasury yields rising toward 1.9% (1.75% previously) by the end of the year. The government’s first quarter estimate of U.S. growth will be published on April 29.

Nowcasts from the Atlanta and New York Federal Reserve banks imply that the economy grew by 6.2% in the first quarter relative to the first quarter of 2020, which gives the National Bureau of Economic Research (NBER) the unenviable task of declaring when the recession ended. It’s unenviable because of the distorted nature of the recession, with low-income households in the precarious position of depending on extended unemployment benefits, while high-income households were subjected to the same horrors of the pandemic, but from an economic standpoint, perhaps only inconvenienced.

Those GDP gains are relative to the very low output of last year and subject to the global race between vaccinations and a mutating coronavirus. Despite those gains, there is still a long way before the economy reaches its potential. And then there is the shake-out of industries and employment that are not likely to survive the recession and uncertainties regarding the politics that will shape the size and scope of the proposed fiscal stimulus.

Nevertheless, there are arguably enough positive indications to begin planning for a return to normal commercial activity. Here is a sampling of what’s to come, or better put, what the data is suggesting.

March RSM US Middle Market Business Index

The March RSM US Middle Market Business Index’s forward-looking expectations on the economy (70%), gross revenues (70%), net earnings (69%), cap ex (55%), hiring (59%) and compensation (59%) all point to robust growth in the real economy over the next six months. If there is one major takeaway from the March monthly survey, it is that middle market hiring and investment are set to accelerate: the percentages of respondents reporting plans to increase staff and make productivity-enhancing capital expenditures over the next six months posted record survey highs.

While the monthly top-line increase in the RSM Middle Market Business Index to 127.4 from 122.4 in February is impressive, the forward view is even more encouraging. Executives’ robust assessment of economic conditions, revenues, earnings, hiring, compensation and capital expenditures over the next six months underscores our position that the U.S. economy will experience a boom in 2021 that will likely unleash the strongest period of American growth since the late 1980s, and quite possibly, the post-World War II period.

Beneath the top-line data, we can infer that growing confidence in economic prospects linked to rising vaccinations, and the fiscal floor put underneath the economy over the past year has bolstered middle market business confidence and is shaping expectations of changing behavior in the short term that will boost economic activity. From our vantage point, the $908 billion in fiscal aid put forward at the end of 2020 and the recent $1.9 trillion American Rescue Plan now working its way through the economy are creating conditions for a multiyear period of strong economic growth.

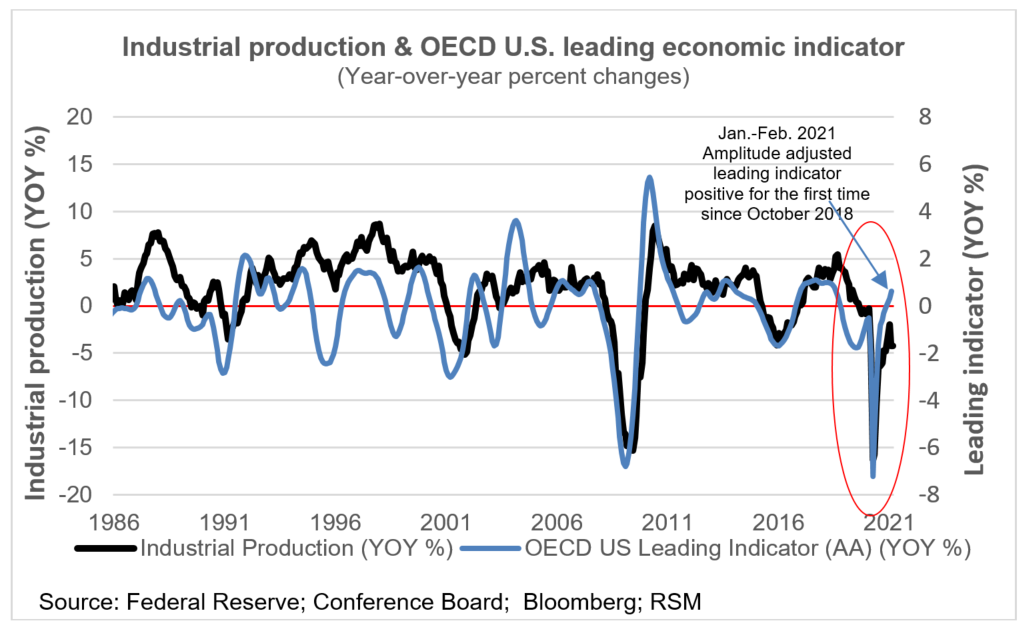

Leading indicators and industrial production

One of the OECD’s leading indicators of the U.S. economy turned positive in January for the first time since February 2020. Both the leading indicator and U.S. industrial production have been in decline since 2018, so this break in the downturn is significant in terms of building confidence in the ability of the economy to survive the global manufacturing recession of 2018-20 and the pandemic of 2020-21.

The decline in industrial production has clearly been decelerating, but it has struggled to show positive yearly growth during the pandemic. Some of that can be attributed to:

- the effect of the energy glut during the pandemic,

- the severe winter storms that crippled much of the U.S., and

- diminished global demand for Boeing aircraft, the mainstay of the U.S. export sector.

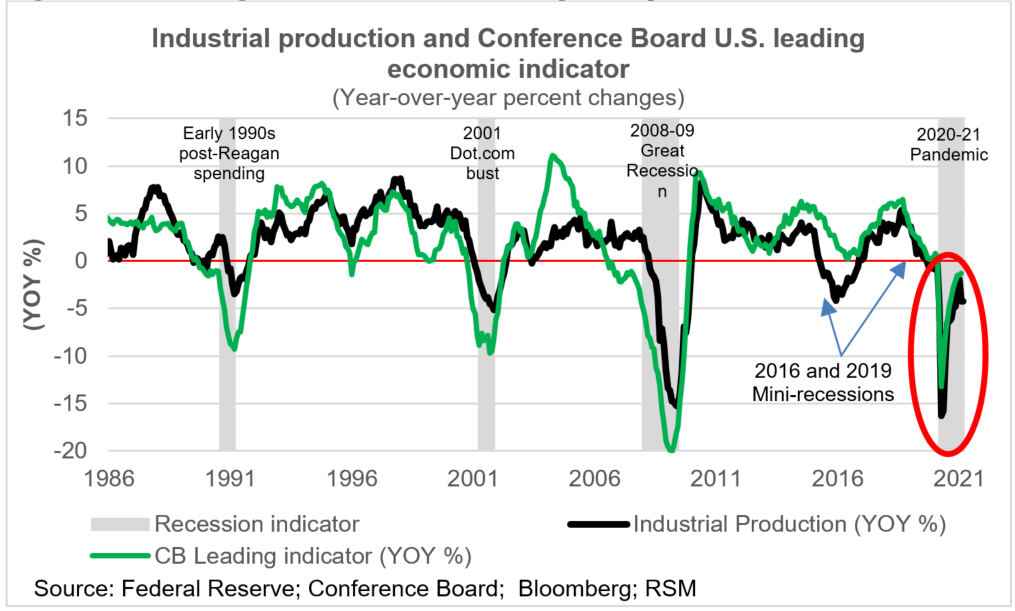

The Conference Board’s leading economic indicator is showing a deceleration in the decline of industrial production through February as well, but the growth rate remains negative. Expectations for increased manufacturing – against a background of a successful vaccination program and the reopening of local economies – suggests the eventuality of positive growth in coming months, particularly due to base-period effects.

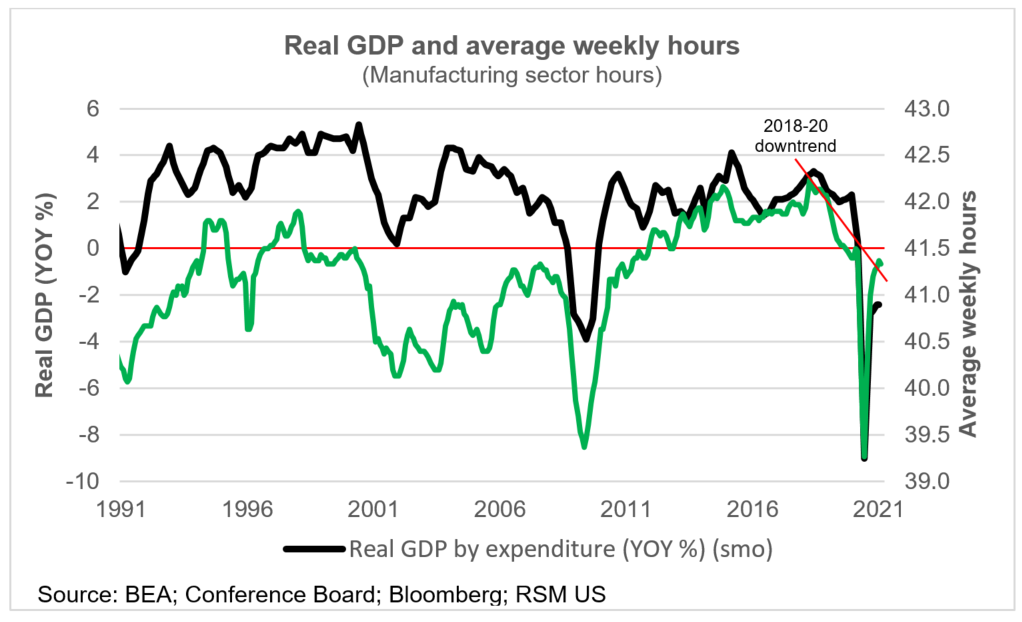

Manufacturing

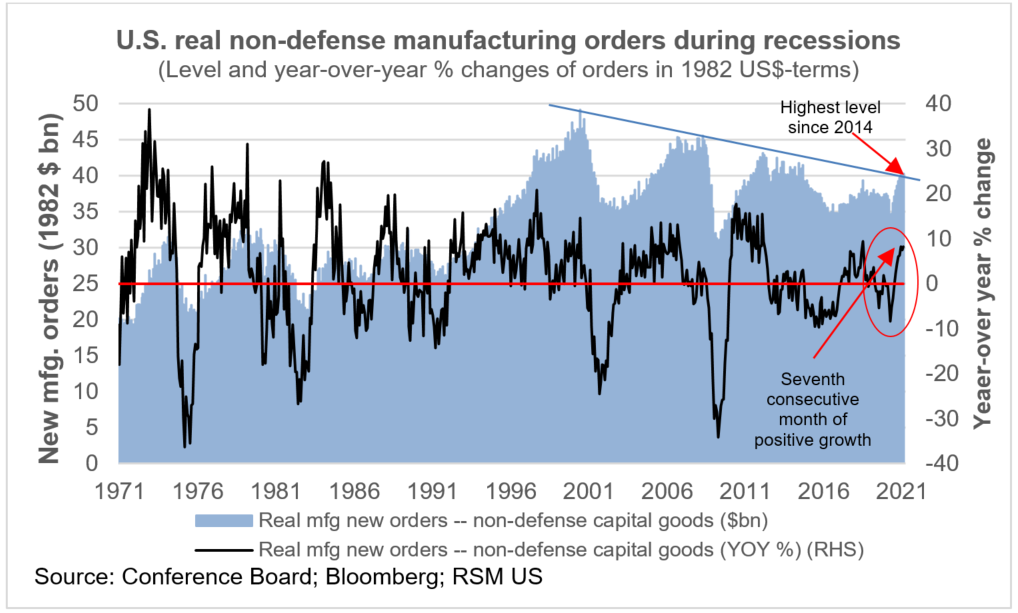

One of the components of the Conference Board’s leading economic indicator is real (inflation-adjusted) nondefense manufacturing orders, which are at their highest level since 2014, and growing at an average rate of 8% per year over the past three months.

We consider manufacturing orders an important indication of growth. They represent confidence expressed through actual money being put down. As our analysis shows, the level of real nondefense orders has been in a long-term decline since early 2000. Because of the downstream ripple effects of manufacturing, a breakthrough of that long-term downtrend would be a significant indication of a sustained recovery.

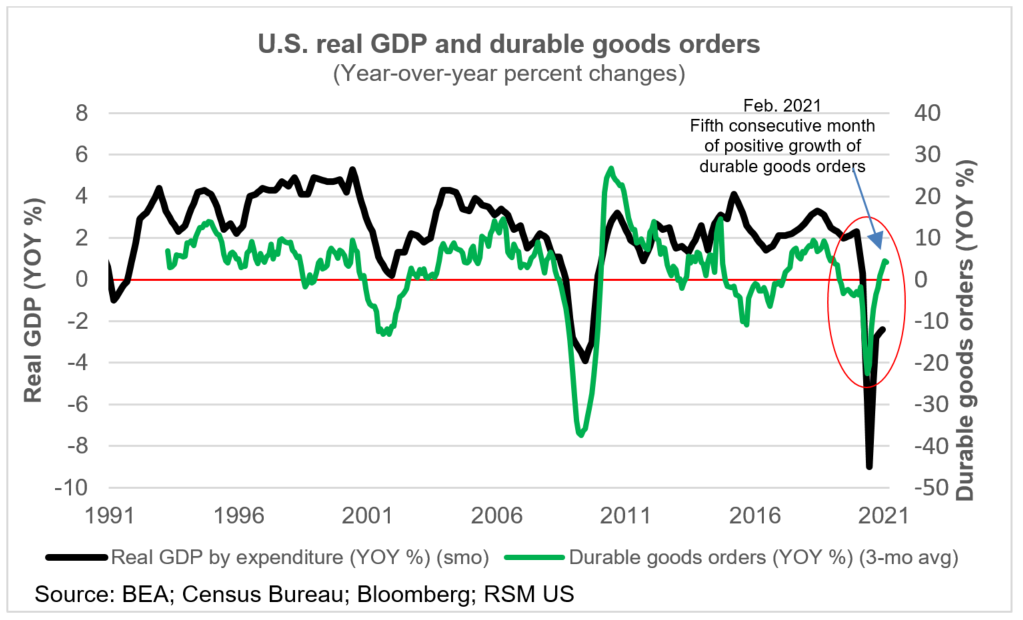

The resurgence of manufacturing is echoed by the increase in sentiment reported by manufacturers and the 4% year-over-year growth of durable goods orders reported during December through February. Manufacturing shipments in January and February grew at an average yearly rate of 1.8%, all according to the Census Bureau.

Another indication is the increase in average number of hours worked to above 41 hours per week in manufacturing. That implies overtime and the potential for additional hiring if the demand for manufactured goods continues to increase.

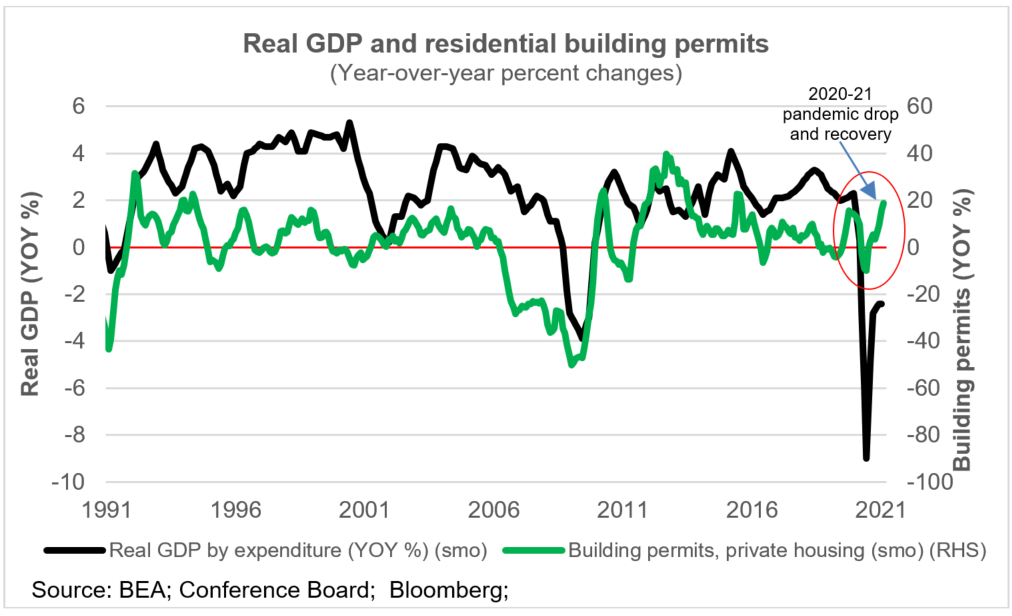

Construction

Residential construction remains strong and we expect it to be one of the primary growth narratives in the early portion of the recovery. The proposed infrastructure plan includes public works construction to rebuild the transportation and energy system, provide universal broadband coverage, and retrofit schools, public buildings and private homes. If passed, it will clearly bolster overall construction activity going forward into 2022 and 2023. Construction jobs will also rebuild household financial balance sheets and increase the demand for new housing, which is already growing at a yearly rate of 20% over the past three months through February.

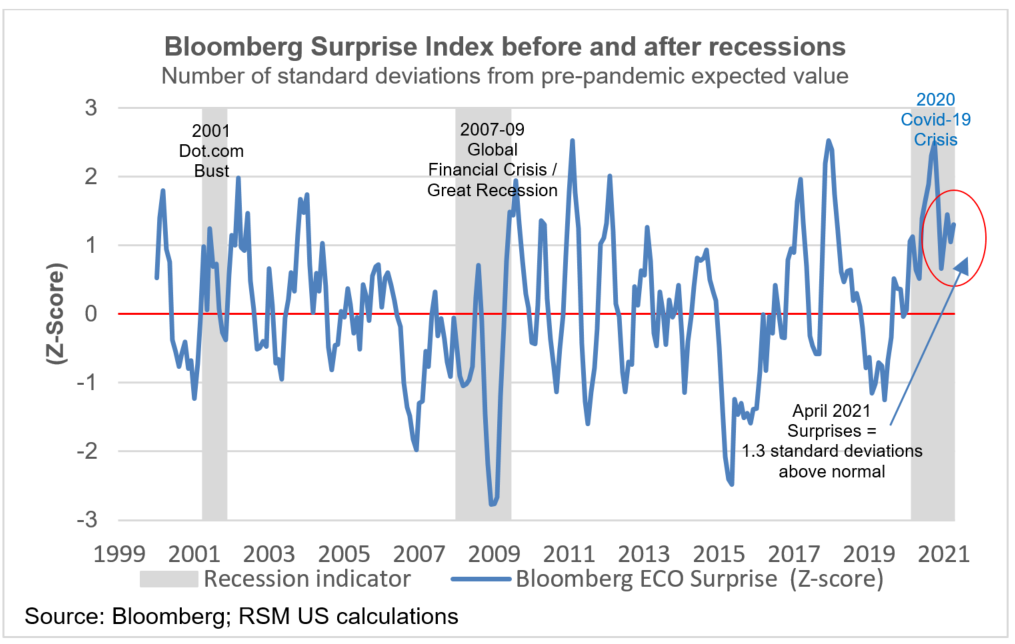

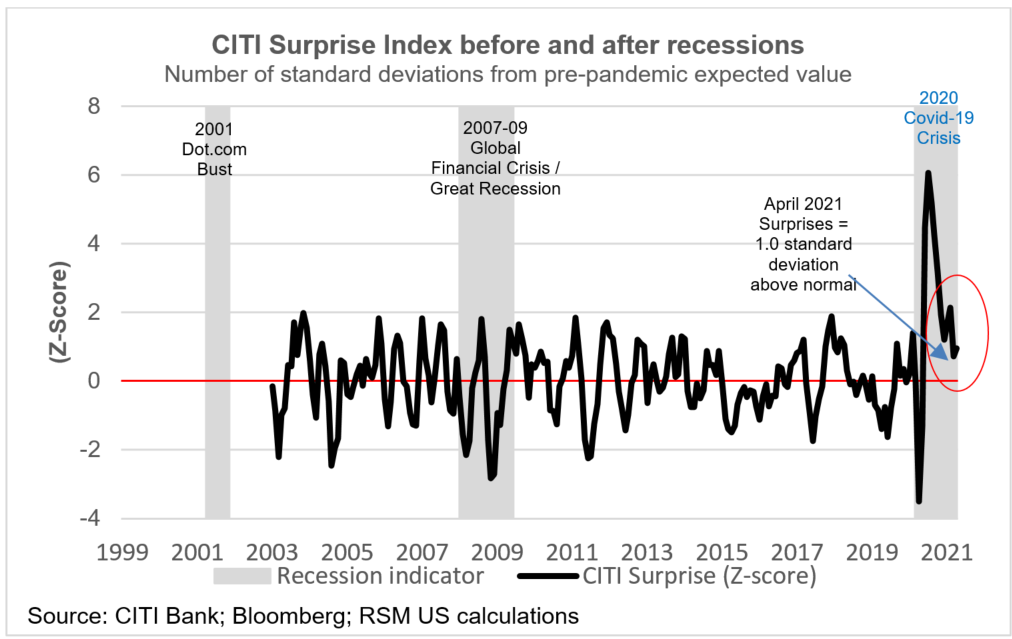

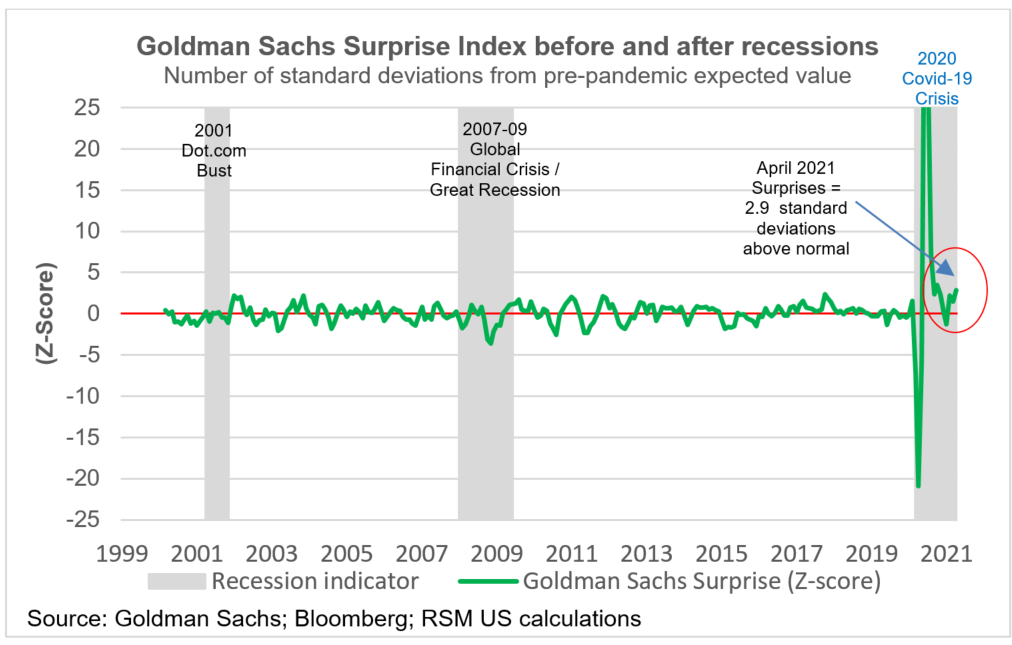

Economic surprise indices

Economic “surprise indices” are measures of the divergence between the expectations of analysts for the release of economic data and the actual values of that data. For example, if analyst expectations for GDP growth call for 3% and the actual value is 4%, that would be a one percentage-point positive surprise, meaning that growth was higher than expected. If actual GDP growth turns out to be only 2%, then that would be a one percentage-point negative surprise.

In general, and because people tend to base their expectations on current conditions, we would expect negative surprises to occur at the end of business-cycle upswings, as analysts hold on to their optimism a little too long. Conversely, we would expect positive surprises to occur at the end of business cycle downturns, with analysts holding onto their pessimism a little too long.

If our hypothesis is correct that the economy has bottomed out, then positive economic surprises are more likely to be prevalent than negative surprises. That is, we think the data in the months ahead will come in better than previously thought reasonable.

Bloomberg, Citi, and Goldman Sachs have each developed Economic Surprise Indices that have more to do with changes in financial assets than with the overall business cycle. But they are notable, in that they show that positive surprises peaked at the height of the pandemic.

They also confirm the inequality of the economic collapse. High earners were able to work and spend at home and kept parts of the economy in the black. That eventually turned into a rout, as small businesses began to fold, and the surprises became less positive.

Since the start of the year, as the vaccination program took off, the surprises appear to be moving higher again, hinting at actual growth exceeding expectations.

For more information on how the coronavirus pandemic is affecting midsize businesses, please visit the RSM Coronavirus Resource Center.